An allocation to active management is a cornerstone of nonprofit investment portfolios. It can provide enhanced returns as well as diversification. According to the 2023 NACUBO-Commonfund Study of Endowments, university endowment portfolios have more than 80% of their assets invested with active managers. And it’s not just for the largest of the large; for endowments with less than $500 million, active management represents 67% of the allocation. These allocations are across all asset classes including equity, fixed income, and alternatives.

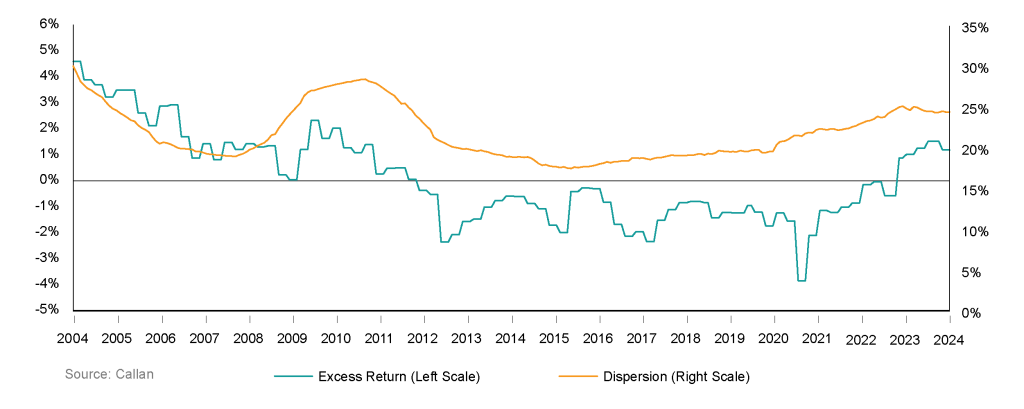

The returns of any portfolio can be enhanced with the selection of skilled active managers. However, history has shown us that some periods have been more favorable for active managers than others. The period beginning in 2012 up to today has been difficult for active management, especially in U.S. equity. If we had a magic 8-Ball that could tell us when to allocate to active managers and when to stick with indexing, our long-term track records would be improved. Since we do not, we will explore market measures that can provide some insight.

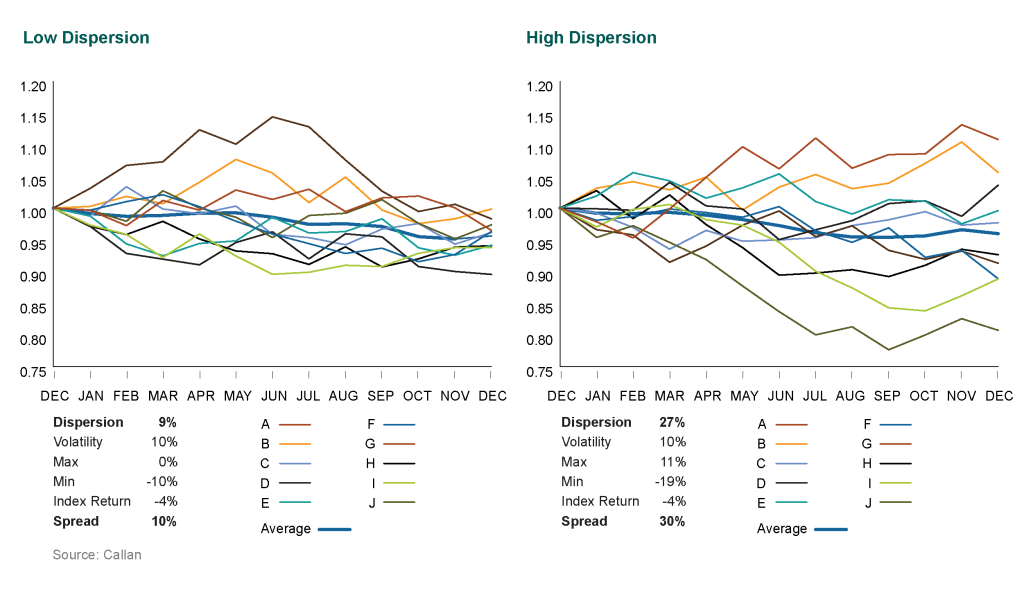

For active management to work, there needs to be a payoff for picking better stocks than the average. The magnitude of that payoff can be measured by equity dispersion. Put another way, it is the value the markets are offering for one’s intelligence as a stock picker.

What is dispersion?

Dispersion measures the spread of returns around the average. Each day indices like the S&P 500 calculate a return that is the market cap-weighted average of the returns of the individual ![]() stocks in the index. But this return figure tells us nothing about the range of returns of individual stocks and hence the opportunity set for stock picking. The measure of this range is dispersion.

stocks in the index. But this return figure tells us nothing about the range of returns of individual stocks and hence the opportunity set for stock picking. The measure of this range is dispersion.

Another way to conceptualize dispersion is to shoot five arrows at a target. A skilled archer will put all five arrows on the bullseye, splitting each arrow with each subsequent shot. On the other hand, your humble author is not such a great shot and may spray the arrows all over the target. The skilled archer has a grouping of arrows with zero dispersion; my dispersion, on the other hand, is very high.