You are currently viewing this website using the Internet Explorer (IE) web browser. This website has limited functionality in IE, and you won’t be able to download research documents. For an optimal experience, please access this website using any other supported web browser.

Listen to This Blog Post

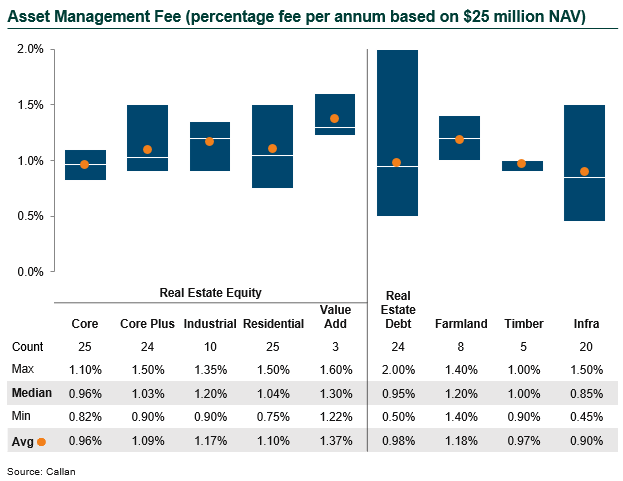

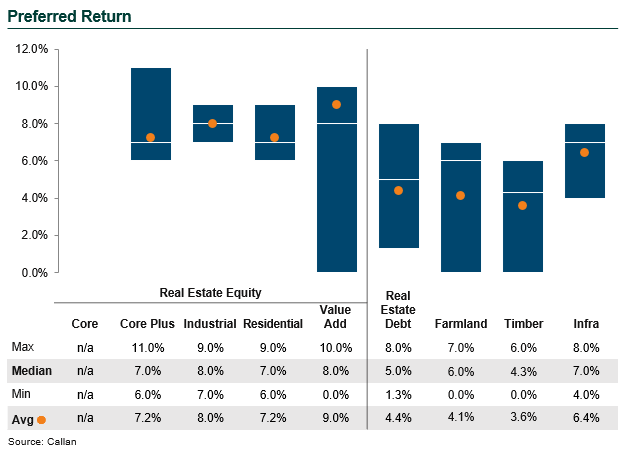

I recently prepared Callan’s 2024 Real Assets Open-End Funds Fees and Terms Study, our inaugural look at these private markets vehicles.

The study included 144 funds, representing offerings across real estate, infrastructure, farmland, and timberland. Of the funds in the study, 77% were real estate funds, and the majority of those were equity funds. Infrastructure funds, at 14% of the data set, were the second-most prevalent. By strategy type, the funds were roughly evenly split between core, core plus, debt, and residential, with a smattering of value-add and industrial funds.

My study focused on four key principal terms:

The full study is available at the link above; this blog post summarizes its key findings.

This study, which will be updated in future years, is intended to help institutional investors better evaluate open-end real assets funds, serving as an industry benchmark when comparing a fund’s terms to its peers. This study can also be useful for real assets investment managers, to determine how their fees and terms compare to other funds.

Disclosures

The Callan Institute (the “Institute”) is, and will be, the sole owner and copyright holder of all material prepared or developed by the Institute. No party has the right to reproduce, revise, resell, disseminate externally, disseminate to any affiliate firms, or post on internal websites any part of any material prepared or developed by the Institute, without the Institute’s permission. Institute clients only have the right to utilize such material internally in their business.

For Investment Managers & Advisers

You are now leaving Callan LLC’s website and going to Callan Family Office’s website. Callan Family Office is not affiliated with Callan LLC. Callan LLC has licensed the Callan® trademark to Callan Family Office for use in providing investment advisory services to ultra-high net worth clients, family foundations, and endowments. Callan Family Office and Callan LLC are independent, unaffiliated investment advisory firms separately registered with the Securities and Exchange Commission under the Investment Advisers Act of 1940.

Callan LLC is not responsible for the services and content on Callan Family Office’s website. Inclusion of this link does not constitute or imply an endorsement, sponsorship, or recommendation by Callan LLC of their website, or its contents, and Callan LLC is not responsible or liable for your use of it. When visiting their website, you are subject to Callan Family Office’s terms of use and privacy policies.