You are currently viewing this website using the Internet Explorer (IE) web browser. This website has limited functionality in IE, and you won’t be able to download research documents. For an optimal experience, please access this website using any other supported web browser.

Listen to This Blog Post

In my recent white paper, available at the link above, I explored the role of private equity secondary investments in institutional portfolios, analyzing their risk-return trade-offs compared to primary private equity funds. This blog post summarizes that work.

Secondary investments involve acquiring interests in already established private equity funds, offering benefits such as diversification, shorter duration, and faster capital distribution. However, they typically yield lower long-term returns than primary partnerships.

The secondary market has grown significantly, with fundraising reaching $100 billion in 2024, up from $22 billion in 2014. This expansion reflects increasing investor interest in liquidity management.

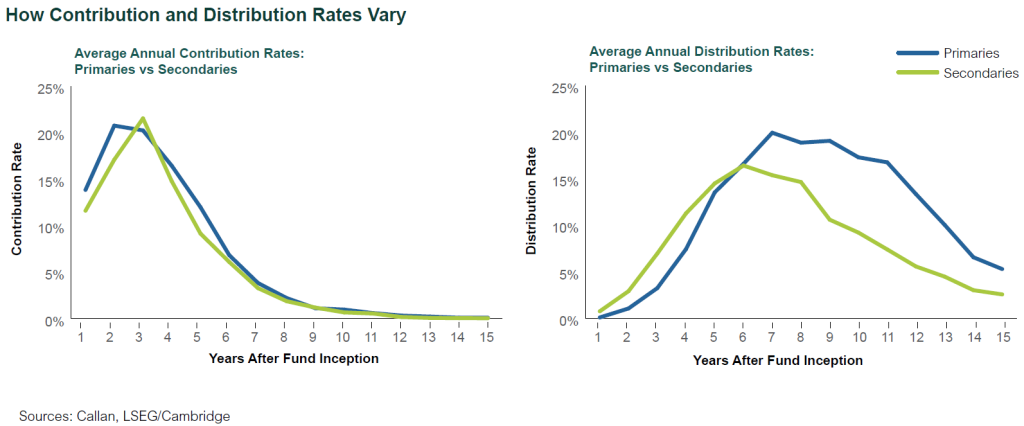

Primary and secondary private equity funds differ in cash flow timing and risk-return profiles.

1) Capital Contributions and Distributions:

2) Appreciation and the J-Curve Effect:

3) Net Asset Value (NAV) Development:

Internal rate of return (IRR) and total value to paid-in capital (TVPI) metrics reveal key differences between primary and secondary funds.

1) IRR Performance:

2) TVPI Performance:

3) Risk-Adjusted Performance:

Investors use secondary funds in different ways within private equity portfolios.

Disclosures

The Callan Institute (the “Institute”) is, and will be, the sole owner and copyright holder of all material prepared or developed by the Institute. No party has the right to reproduce, revise, resell, disseminate externally, disseminate to any affiliate firms, or post on internal websites any part of any material prepared or developed by the Institute, without the Institute’s permission. Institute clients only have the right to utilize such material internally in their business.

For Investment Managers & Advisers

You are now leaving Callan LLC’s website and going to Callan Family Office’s website. Callan Family Office is not affiliated with Callan LLC. Callan LLC has licensed the Callan® trademark to Callan Family Office for use in providing investment advisory services to ultra-high net worth clients, family foundations, and endowments. Callan Family Office and Callan LLC are independent, unaffiliated investment advisory firms separately registered with the Securities and Exchange Commission under the Investment Advisers Act of 1940.

Callan LLC is not responsible for the services and content on Callan Family Office’s website. Inclusion of this link does not constitute or imply an endorsement, sponsorship, or recommendation by Callan LLC of their website, or its contents, and Callan LLC is not responsible or liable for your use of it. When visiting their website, you are subject to Callan Family Office’s terms of use and privacy policies.