Institutional investors have long been wary of sequence-of-returns risk, the possibility that the timing of bad short-term returns could harm outcomes even if the portfolio’s expected returns are achieved by the end of a long-term investment horizon.

This blog post, one in a series, is based on my recent paper on this risk, available at the link above. Other blog posts in the series will be available here.

Both the type of return used and the outcome an institutional investor cares about can vary widely by type of investor. An institutional investor can analyze Monte Carlo simulations of the appropriate types of long-term return and key outcomes to show whether possible long-term returns align with long-term outcomes.

Quantifying Sequence-of-Returns Risk

The sequence-of-returns risk can then be quantified using Spearman’s rank correlation, a close cousin of the “standard” Pearson correlation that is commonly used by institutional investors. A correlation of 1 indicates that there is no sequence-of-returns risk because long-term outcomes display total concordance with long-term returns.

This scenario, which is admittedly unrealistic for most types of investors, involves portfolios with no inflows or outflows. Lower correlation between long-term returns and long-term outcomes indicates greater sequence-of-returns risk.

Analyzing sequence-of-returns risk does not replace other tools used to evaluate asset-allocation risks but provides complementary analysis. And for some institutional investors, especially those with a high probability of depleting assets, sequence-of-returns risk may be outsized—and they ignore it at their peril and that of their beneficiaries.

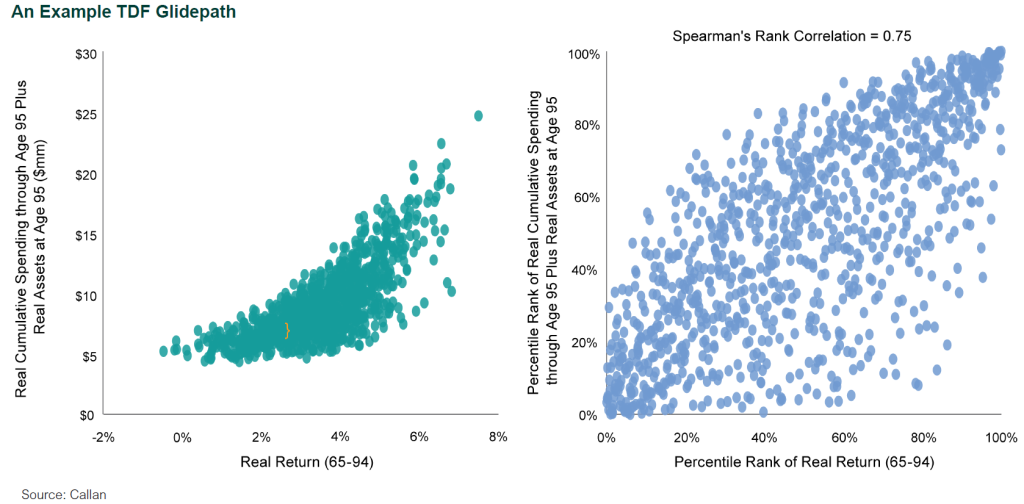

How to Quantify Sequence-of-Returns Risk for a TDF Glidepath

An example target date fund glidepath of a defined contribution (DC) plan client of Callan is shown in the chart below. Longevity risk is an important consideration for participants in TDFs and the plan sponsors that oversee the glidepaths of such funds. A common metric for longevity risk is the probability that participants will spend their entire nest egg if they live to different ages. This concept can be extended to both the amount a retiree is able to spend in retirement over a given horizon, such as 30 years, and their ending asset balance. Participants may wish to maintain real (inflation-adjusted) spending through retirement; therefore, it may be appropriate to adjust these values for inflation and add them together for a metric called ultimate real purchasing power, then compare them against real return.

In this example, only post-retirement experience is simulated to analyze the impact of post-retirement investment decisions on a hypothetical participant retiring at 65. For 25-year-old participants just starting their careers, outcomes will be heavily impacted by pre-retirement experience. Conditioned on a real return of 2%, the TDF glidepath in the chart would have an expected ultimate real purchasing power of $6.4 million and a standard deviation of $807,000, as shown in orange.

Disclosures

The Callan Institute (the “Institute”) is, and will be, the sole owner and copyright holder of all material prepared or developed by the Institute. No party has the right to reproduce, revise, resell, disseminate externally, disseminate to any affiliate firms, or post on internal websites any part of any material prepared or developed by the Institute, without the Institute’s permission. Institute clients only have the right to utilize such material internally in their business.